New Delhi: India relies on imports for around 90% of its metallurgical (met) coal requirements, and that dependence is set to deepen. The country aims to reach 300 million tonnes per annum (MTPA) of crude steel capacity by 2030, with 64% of the steel capacity under development reliant on coal-based blast furnace (BF) technology that requires imported met coal.

A new briefing note by the Institute for Energy Economics and Financial Analysis (IEEFA), ‘US met coal offers limited relief for India’s steel energy security’, finds that India’s push to diversify met coal imports toward the US, backed by recent bilateral trade engagement and heightened energy security concerns following the West Asia conflict, is unlikely to reduce these risks. Global price linkages, higher freight costs, limited US export capacity, and technical constraints in Indian steel plants all undercut the case for US coal as a meaningful substitute.

Australian supply still drives global prices

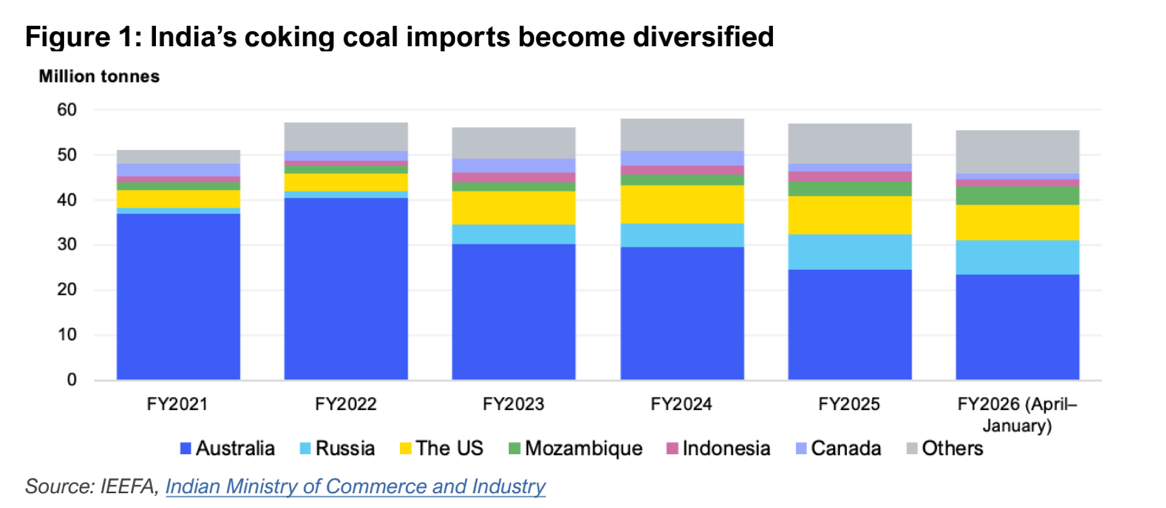

While India has broadened its supplier base in recent years, Australia continues to account for nearly half of global seaborne met coal exports. That dominance means supply disruptions in Australia can trigger price spikes across the entire market, including for US-origin coal. For instance, January 2026 saw heavy rainfall and flooding in Queensland, the world’s most significant met coal exporting region, disrupting mining operations and logistics. The resulting supply disruption drove up prices, with benchmark premium Australian hard coking coal (HCC) surging to USD252.5 per tonne (INR23,404 per tonne) on 4 February, an 18-month high and up more than 50% from the lows seen in March 2025.

Freight costs and declining US capacity limit substitution

The growing role of US coal in India’s import mix has been supported by shifting trade patterns and recent bilateral agreements. However, US coal faces structural disadvantages. Australian coal benefits from significantly shorter shipping distances to India, resulting in lower freight costs. US cargoes travel much longer routes, adding transportation costs that erode competitiveness.

“Freight economics are a key factor. The longer distance for US cargoes means higher freight costs, now exacerbated by the West Asia crisis and the impact on shipping fuel,” says Simon Nicholas, co-author of the briefing note, and Global Lead Analyst – Steel at IEEFA.

US export capacity is also limited and expected to decline in the coming years, even as India’s demand continues to rise. This imbalance reduces the potential for US coal to serve as a reliable long-term substitute.

Moreover, Indian steelmakers are increasingly adopting stamp-charging technology, a coking process optimised for blends of domestic and Australian coal. This further limits the suitability of US-origin coal in many existing plants and raises the cost of switching suppliers.

Reducing import dependence

The analysis concludes that diversification alone cannot address India’s underlying energy security risks.

“Even with diversified supply, India will remain exposed to global price volatility, supply disruptions, and climate-related risks in major exporting regions,” says the note’s co-author Saumya Nautiyal, Energy Finance Analyst – South Asia, IEEFA.

IEEFA recommends accelerating the transition to scrap-based electric arc furnace steelmaking and scaling up green hydrogen-based production. Domestic green hydrogen, in particular, is emerging as a strategic opportunity in the context of fossil fuel market instability and geopolitical risks. By reducing long-term dependence on imported met coal, India can build a more resilient and competitive steel sector aligned with its energy security and decarbonisation goals.