New Delhi: India’s steel and aluminium exports to the European Union (EU) fell 24.4% in financial year (FY) 2025, with steel alone down 35.1%, before any Carbon Border Adjustment Mechanism (CBAM) financial obligation had taken effect. The decline, which suggests European buyers are already reorienting toward lower-emission producers, underscores what is at stake as India’s Carbon Credit Trading Scheme (CCTS) enters its operational phase. Over the next two to five years, choices made by regulators, policymakers, and market participants on market architecture, compliance obligations, and price formation will shape how far the CCTS develops into a market capable of guiding capital-intensive industrial investment over 15- to 30-year horizons.

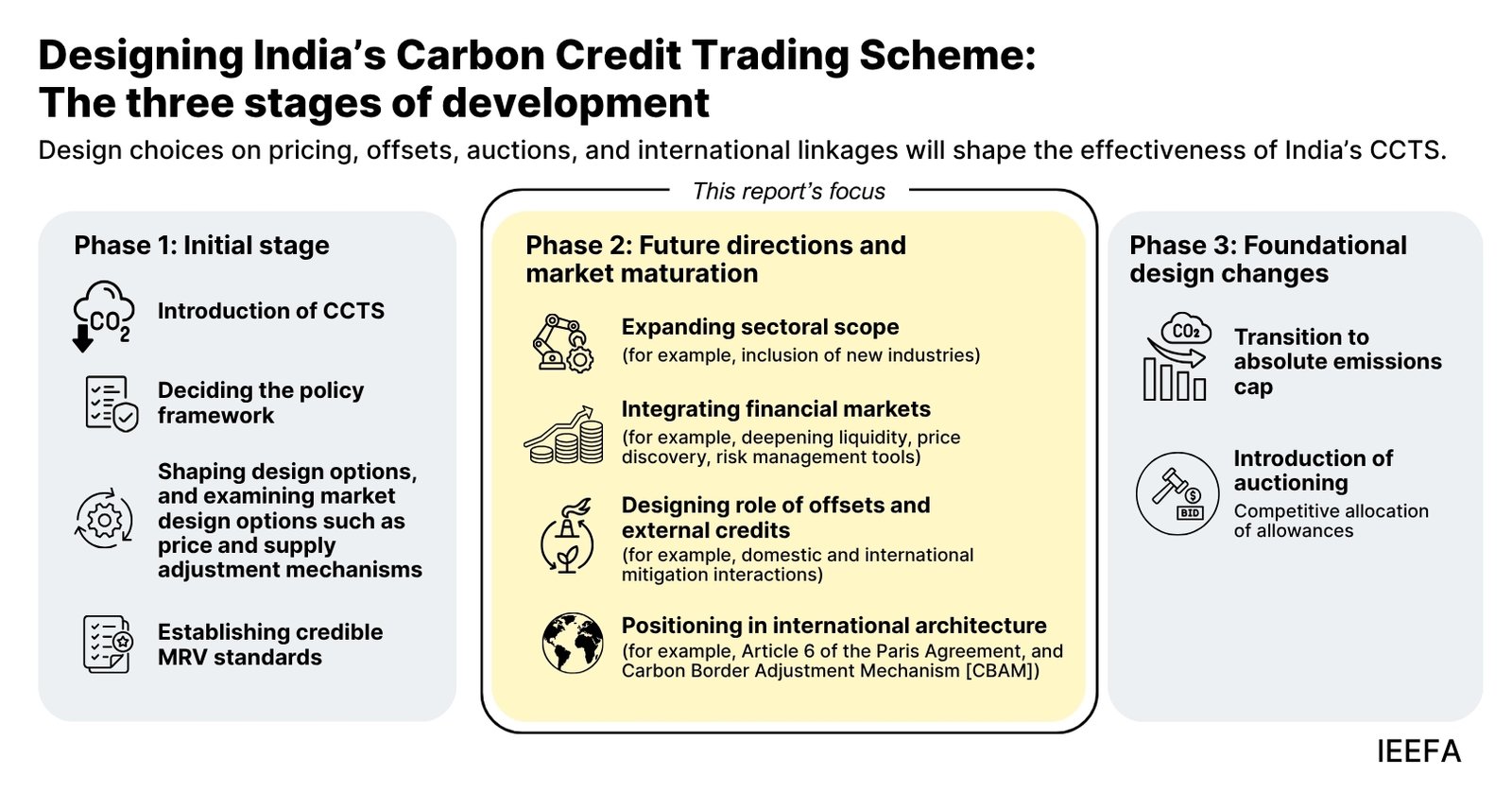

A new report by the Institute for Energy Economics and Financial Analysis (IEEFA), ‘The road ahead for India’s Carbon Credit Trading Scheme’, produced in collaboration with the Environmental Defense Fund (EDF), maps the trajectory of this next phase and makes recommendations on the decisions that will shape the scheme’s trajectory. The analysis is structured around four interconnected themes: financial market participation; the design choices India faces in responding to border carbon costs, of which CBAM is the most prominent; sectoral expansion, including the implications of incorporating the power sector; and managing offsets and Article 6 (of the Paris Agreement) opportunities while safeguarding the integrity of India’s carbon market and sovereign mitigation goals.

The report draws on experience from comparable systems. In Korea, restricting early participation to compliance entities, alongside a surplus of allowances, left trading thin and prices subdued in the scheme’s initial years. India’s own Perform, Achieve and Trade (PAT) scheme, an important step in building market experience, saw certificate trading fall short of the volumes mandated. Both point to the same lesson: market depth and price signals depend first on whether targets create genuine compliance pressure, and then on whether that pressure is consistently maintained.

“Every major emissions trading system (ETS) began with compliance entities only. The CCTS is right to do the same. Financial intermediaries matter eventually for what they make possible: continuous price discovery and the hedging that gives firms confidence to commit to large decarbonisation investments over long horizons. A market that only settles positions around compliance deadlines would struggle to provide that. The precondition for financial intermediaries’ inclusion is genuine scarcity and credible enforcement, and that is what the CCTS needs to establish first,” says Saurabh Trivedi, co-author of the report and Lead Specialist, Sustainable Finance and Carbon Markets at IEEFA, South Asia.

On CBAM, the report cites figures reported in the media showing that India’s steel and aluminium exports to the EU fell 24.4% in financial year (FY) 2025 before any financial obligation had taken effect, with steel alone down 35.1%, suggesting European buyers are already reorienting toward lower-emission producers. Irrespective of the ongoing international discussions around CBAM, the report’s focus on domestic market design.

“What matters now is how the EU’s recognition of carbon prices paid in third countries will interact with India’s market design, and how the CCTS can be calibrated so that domestic carbon costs are credited at the border. A stronger domestic carbon market supports industrial competitiveness and helps ensure that more of any carbon value is recognised and retained within India. International experience points to the design choices that make that possible, from benchmark calibration to the eventual role of auctioning, which India can consider over time in step with its own priorities,” says co-author Subham Shrivastava, a climate finance analyst and consultant at IEEFA.

The power sector accounts for nearly 40% of India’s greenhouse gas emissions but is not part of the initial compliance boundary, a deliberate sequencing choice that draws in industrial sectors first while the power sector carries structural and transitional complexities of its own. As the scheme evolves, greater clarity on how and when the sector might be integrated will become increasingly important, given the long operational life of power assets.

“International experience shows that regulated electricity markets can also support carbon pricing. China, for example, launched its ETS with the power sector as its first covered sector despite operating regulated electricity tariffs. India’s electricity sector has several enabling features, including change-in-law provisions in power purchase agreements that can support the recovery of carbon compliance costs. As the CCTS matures, future integration of the power sector will benefit from careful consideration of electricity market regulation, dispatch decisions, cost recovery mechanisms, and coordination between carbon market and electricity regulators,” says Saloni Sachdeva Michael, Energy Specialist, India Clean Energy Transition at IEEFA, South Asia, and a co-author of the report.

The report also takes up the sequencing of offsets and India’s opportunities under Article 6 of the Paris Agreement, cautioning that these are best developed once the compliance market has found its footing. “Offsets are best sequenced to follow market conditions, rather than lead them,” says Shrivastava. “International experience suggests India’s most valuable opportunity lies in authorising high-integrity mitigation outcomes under Article 6, particularly for higher-cost emissions reduction. This would draw in international finance for reductions that might not otherwise happen, while the cheaper reductions India needs for its own targets stay at home. Domestic offset integration can then be designed for a later stage, once the compliance market has established a credible price and built a foundation of high-integrity credits.”

The foundations of a functioning carbon market remain the priority, but the more advanced features benefit from early design: financial integration, power sector inclusion, alignment with border carbon measures, and a coherent offset architecture all take time to develop well. India is at the stage where those choices are still open, and the choices made now will define the market’s trajectory for years to come.