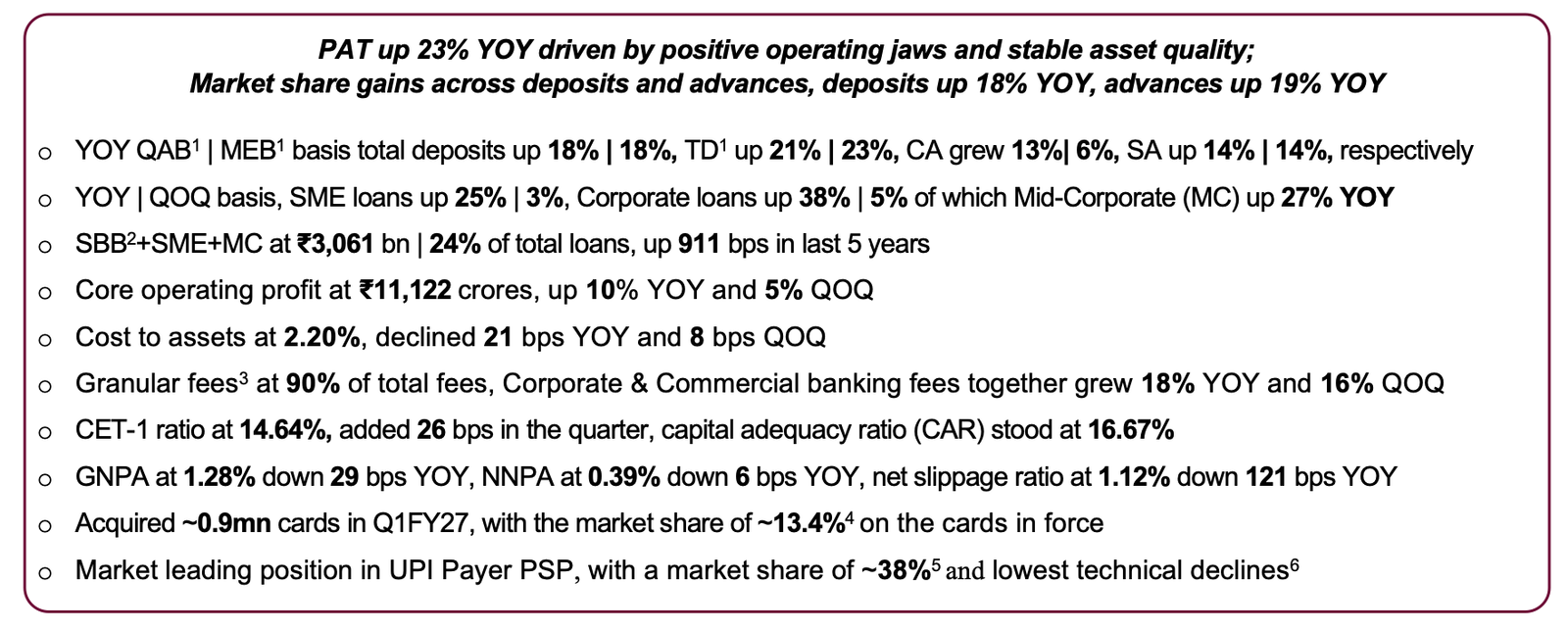

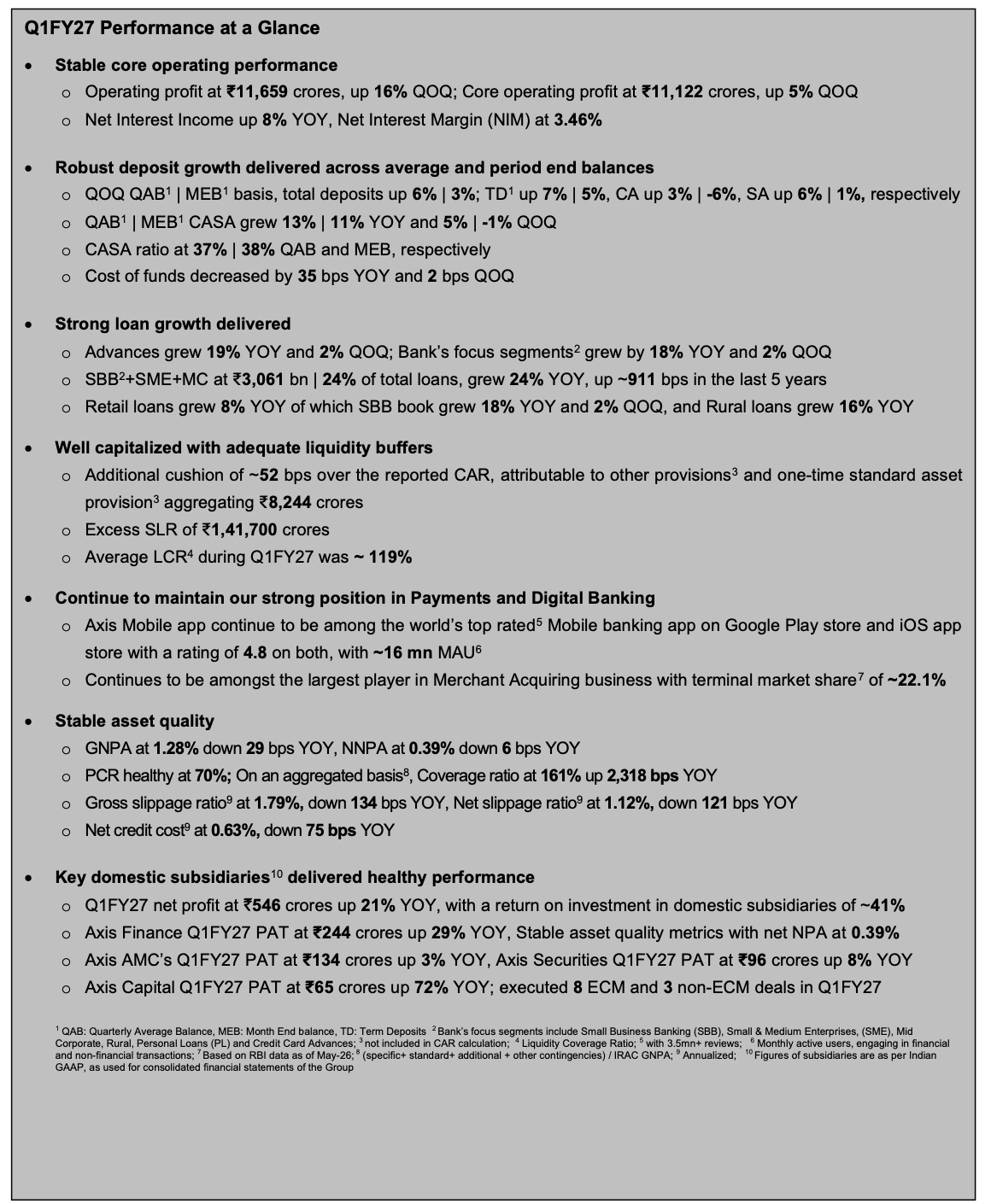

New Delhi: The Axis Bank on Saturday announced its financial results for the quarter ended Jone 30, 2026. The Bank’s Net Interest Income (NII) for Q1FY27 stood at `14,646 crores up 8% YOY basis. Net Interest Margin (NIM) for Q1FY27 stood at 3.46%.

Other Income

Fee income for Q1FY27 grew 7% YOY to `6,156 crores. Retail fees grew 2% YOY, constituted 67% of the Bank’s total fee income. The Corporate & Commercial banking fees together grew 18% YOY and 16% QOQ to `2,004 crores. The trading income for the quarter stood at `537 crores; miscellaneous income in Q1FY27 stood at `42 crores. Overall, non-interest income (comprising of fee, trading and miscellaneous income) for Q1FY27 stood at `6,735 crores.

Operating Profit and Net Profit

The Bank’s operating profit for the quarter stood at `11,659 crores. Core operating profit stood at `11,122 crores. Operating cost grew 5% YOY in Q1FY27. Net profit up 23% YOY to `7,114 crores in Q1FY27.

Provisions and contingencies

Provision and contingencies for Q1FY27 stood at `2,223 crores. Specific loan loss provisions for Q1FY27 stood at `2,079 crores. The Bank holds cumulative provisions (standard + additional other than NPA) of `15,608 crores as on June 30, 2026. It is pertinent to note that this is over and above the NPA provisioning included in our PCR calculations. These cumulative provisions translate to a standard asset coverage of 1.24% as on 30th June 2026. On an aggregated basis, our provision coverage ratio (including specific + standard + additional) stands at 161% of GNPA as on 30th June 2026. Credit cost (annualized) for the quarter ended 30th June 2026 stood at 0.63%.

During Q4 of FY26, the Bank had proactively strengthened its balance sheet by voluntarily enhancing its prudent provisioning framework for standard assets, in line with our conservative risk-management philosophy. Based on an assessment of evolving and unpredictable macroeconomic and geopolitical uncertainties, the Bank had created an additional one-time provision of ₹2,001 crores during Q4FY26. The Bank has not drawn down from the West Asia provision created in Q4FY26 and the said provision continues to remain at ₹2,001 crores at June 30, 2026. This provision continues to be prudent and precautionary in nature and does not reflect any deterioration in asset quality or adverse credit trends in the Bank’s loan or investment portfolio as of the reporting date.

Balance Sheet: As on 30th June 2026

The Bank’s balance sheet grew 20% YOY and stood at `19,21,966 crores as on 30th June 2026. The total deposits grew 3% QOQ and 18% YOY on month end basis, of which current account deposits grew 6% YOY, saving account deposits grew 14% YOY and term deposits 23% YOY. The share of CASA deposits in total deposits stood at 38%. On QAB basis, total deposits grew 6% QOQ and 18% YOY, within which savings account deposits grew 14% YOY, current account deposits grew 13% YOY, and term deposits grew 21% YOY.

The Bank’s advances grew 19% YOY and 2% QOQ to `12,61,557 crores as on 30th June 2026. Retail loans grew 8% YOY to `6,75,546 crores and accounted for 54% of the net advances of the Bank. The share of secured retail loans1 was ~73%, with home loans comprising 26% of the retail book. Small Business Banking (SBB) grew 2% QOQ and 18% YOY, Loan against property grew 11% YOY, Personal loans grew 7% YOY, Credit card advances grew 5% YOY and Rural loan portfolio grew 16% YOY. SME book remains well diversified across geographies and sectors, grew 3% QOQ and 25% YOY to`1,51,619 crores. Corporate loan book grew 5% QOQ and 38% YOY. Mid-corporate book grew 10% QOQ and 27% YOY. ~91% of corporate book is rated A- and above with 87% of incremental sanctions in Q1FY27 being to corporates rated A- and above.

The book value of the Bank’s investments portfolio as on 30th June 2026, was `4,38,955 crores, of which `3,61,934 crores were in government securities, while `51,938 crores were invested in corporate bonds and `25,083 crores in other securities such as equities, mutual funds, etc. Out of these, 74% are in Held to Maturity (HTM) category, 11% of investments are Available for Sale (AFS), 13% are in Fair Value through Profit & Loss (FVTPL) category and 2% are investments in Subsidiaries and Associate.

Payments and Digital

During Q1FY27, the Bank issued ~0.92 million new credit cards and it continues to remain among the top players in the Retail Digital banking space with:

• 48% – YOY growth in total UPI transaction value,

• 98% – Share of digital transactions in the Bank’s total financial transactions by individual customers,

• 46% – New mutual fund SIPs sourced (by volume) through digital channels,

• 66% – SA accounts opened through tab banking,

• 48% – Individual Retail term deposits (by value) opened digitally, and

• 25% – YOY growth in mobile banking transaction volumes.

The Bank’s focus remains on reimagining end-to-end journeys and transforming the core and becoming a partner of choice for ecosystems. Axis Mobile is among the world’s highest rated mobile banking app on Google Play store and iOS app store with rating of 4.8 on each with over 3.5 million reviews. The Bank’s mobile app continues to see healthy growth, with Monthly Active Users of ~16 million and ~12 million non-Axis Bank customers2 using Axis Mobile.

Axis Bank continues to maintain its market leading position in UPI Payer PSP space with a market share of ~38% by volume3, along with maintaining the lowest technical declines4 among the top 50 UPI Remitter Members. The Bank continue to be amongst the largest players in Merchant Acquiring business in India with a market share5 of 22.1%.

On WhatsApp banking, the Bank now has over 40 million customers on board since its launch in 2021. The Bank has been among the first to go live on Account Aggregator (AA) network and has seen strong initial traction in AA based digital lending. The Bank has 480 APIs hosted on its API Developer Portal.

Wealth Management Business – Burgundy

The Bank’s wealth management business is among the largest in India with assets under management (AUM) of `7,53,819 crores at the end of 30th June 2026 that grew 20% YOY and 11% QOQ. Burgundy Private, the Bank’s proposition for high and ultra-high net worth clients, covers 17,408 families with AUM increasing 16% YOY and 12% QOQ to `2,68,058 crores. Capital Adequacy and Shareholders’ Funds The shareholders’ funds of the Bank grew 15% YOY and stood at `2,11,693 crores as on 30th June 2026. The Capital Adequacy Ratio (CAR) and CET1 ratio stood at 16.67% and 14.64% respectively at the end of 30th June 2026. Additionally, `7,013 crores of other provisions and `1,231 crores of one-time additional standard asset provision, are not considered for CAR calculation, providing cushion of ~52 bps over the reported CAR. The Book value per equity share increased to `681 as on 30th June 2026 from `596 as on 30th June 2025.

Asset Quality

As on 30th June 2026, the Bank’s reported Gross NPA and Net NPA levels were 1.28% and 0.39% respectively, as against 1.57% and 0.45% as on 30th June 2025. Recoveries from written off accounts for the quarter were `961 crores. Reported net slippages in the quarter adjusted for recoveries from written off pool was `2,479 crores, of which retail was `2,614 crores, CBG was `136 crores and Wholesale was negative `271 crores.

Gross slippages during the quarter were `5,566 crores, compared to `4,675 crores in Q4FY26 and `8,200 crores in Q1FY26. Recoveries and upgrades from NPAs during the quarter were `2,126 crores. The Bank in the quarter wrote off NPAs aggregating `2,399 crores.

As on 30th June 2026, the Bank’s provision coverage, as a proportion of Gross NPAs stood at 70%, as compared to 70% as at 31st March 2026 and 71% as at 30th June 2025.

The fund based outstanding of standard restructured loans implemented under resolution framework for COVID-19 related stress (Covid 1.0 and Covid 2.0) declined during the quarter and as at 30th June 2026 stood at `913 crores that translates to 0.07% of the gross customer assets. The Bank carries a provision of ~17% on restructured loans, which is in excess of regulatory limits.

Network

The Bank’s overall distribution network stands at 6,295 domestic branches and extension counters along with 315 Business Correspondent Banking Outlets (BCBOs) situated across 3,352 centers as at 30th June 2026 compared to 5,879 domestic branches and extension counters, and 235 BCBO’s situated in 3,192 centers as at 30th June 2025. As on 30th June 2026, the Bank had 12,564 ATMs and cash recyclers spread across the country. The Bank’s Axis Virtual Centre is present across eight centers with 1,700 Virtual Relationship Managers as on 30th June 2026.