Mumbai: IndoStar Capital Finance, a middle-layer non-banking finance company (NBFC) registered with the Reserve Bank of India, announced its financial results for the quarter and the year ended March 31, 2026 on May 27th, 2026.

IndoStar is a retail NBFC focused on secured lending across Vehicle Finance (VF) and Micro Loans Against Property (M-LAP), targeting the credit needs of underserved segments.

Operational and Financial highlights:

Disbursements for the quarter stood at INR 1,306 crore, reflecting a strong 17% sequential growth over Q3FY26 and

21% growth over Q4FY25.

Assets Under Management (AUM) stood at ₹8,056 crore as of March 31, 2026, registering a 5% increase compared to the previous quarter, supported by growth across both Vehicle Finance and M-LAP segments.

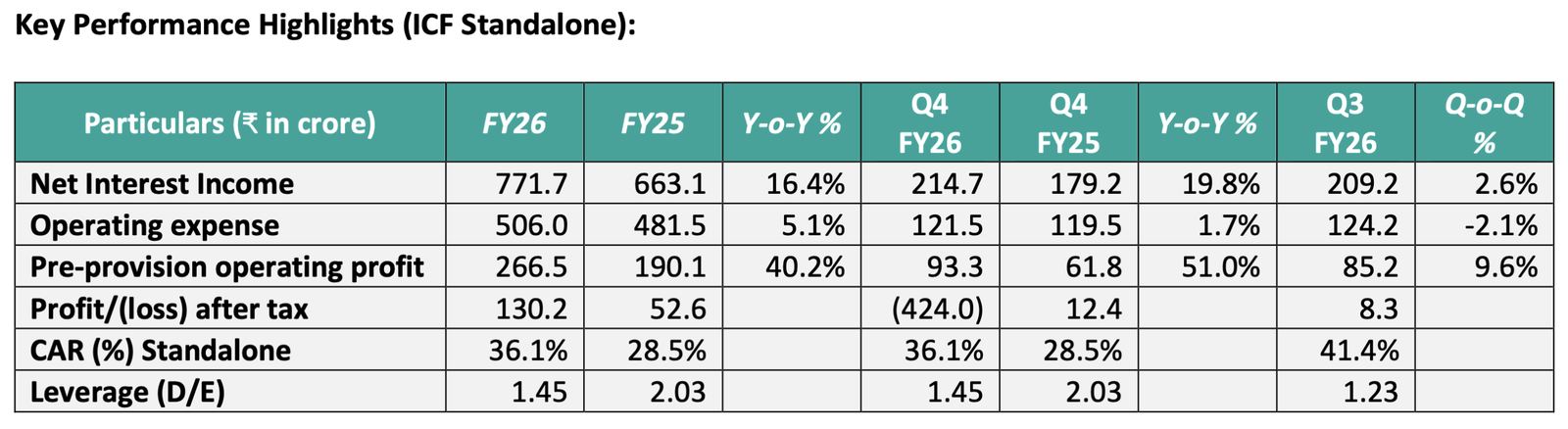

On a standalone basis, Net Interest Income grew by 3% QoQ and 20% YoY, supported by a continued reduction in borrowing costs.

Pre-provision operating profit (PPOP) stood at INR 93 crore, reflecting a growth of 10% QoQ and 51% YoY, driven by improved operating efficiencies.

Over the last few quarters, the company has also witnessed a steady improvement in its borrowing profile, with weighted average cost of funds declining to 10.2% in Q4 FY26 from 11.0% in Q4 FY25, representing an improvement of 80 basis points.

The Company’s asset quality remains stable with Gross Stage 3 assets at 4.77% and Net Stage 3 assets at 2.09% as at March 31, 2026.

Security Receipts and Provisioning

As a decisive step towards completing its initiative to de-risk the balance sheet from potential future volatility arising from the legacy portfolio of Security Receipts (SRs), the Company made an additional provision of ₹326.13 crore against this portfolio.

As of March 31, 2026, the gross carrying value of SRs stood at ₹1,607.78 crore while the net carrying value reduced to ₹588.63 crore from ₹1,022.60 crore as of March 31, 2025. The provision coverage ratio on SRs increased to 63%, compared to 26% a year ago.

The Company maintains strong visibility on recoveries from its SR portfolio, with the current net carrying value of approximately ₹588.63 crore expected to be realized in due course.

Macroeconomic Developments and Management Overlay

During the quarter, geopolitical developments in West Asia introduced heightened macroeconomic uncertainties, particularly through volatility in energy prices and potential supply chain disruptions. Given the evolving nature of these developments and the limited availability of reliable data, the full impact is not yet captured within the Expected Credit Loss (ECL) framework.

As a prudent measure, the management has undertaken a qualitative assessment of potentially exposed portfolios and recognized an additional management overlay of ₹49.00 crore during the quarter. The Company will continue to closely monitor external developments and reassess the adequacy of this overlay in subsequent reporting periods.

The Company maintains strong visibility on recoveries from its SR portfolio, with the current net carrying value of approximately ₹588.63 crore expected to be realized in due course.

Macroeconomic Developments and Management Overlay

During the quarter, geopolitical developments in West Asia introduced heightened macroeconomic uncertainties, particularly through volatility in energy prices and potential supply chain disruptions. Given the evolving nature of these developments and the limited availability of reliable data, the full impact is not yet captured within the Expected Credit Loss (ECL) framework.

As a prudent measure, the management has undertaken a qualitative assessment of potentially exposed portfolios and recognized an additional management overlay of ₹49.00 crore during the quarter. The Company will continue to closely monitor external developments and reassess the adequacy of this overlay in subsequent reporting periods.