Ahmedabad: Adani Ports and Special Economic Zone Limited (APSEZ), India’s largest integrated transport operator, announced its results for the quarter and year ended March 31, 2026.

Performance highlights

FY26 marks an important milestone for APSEZ as we reach a critical scale of operations. Our proven execution capabilities enable us to consistently deliver projects ahead of schedule. The year also underscored the inherent resilience of our business, as we ensured continuity of critical maritime trade amid Middle East conflicts and global trade disruptions due to tariffs. Strong growth in our marine and logistics services reinforces the composite nature of our integrated operating model. As shore-to-door solutions rapidly scale across India, APSEZ is playing an increasingly strategic role in strengthening the country’s logistics efficiency and supply-chain resilience.

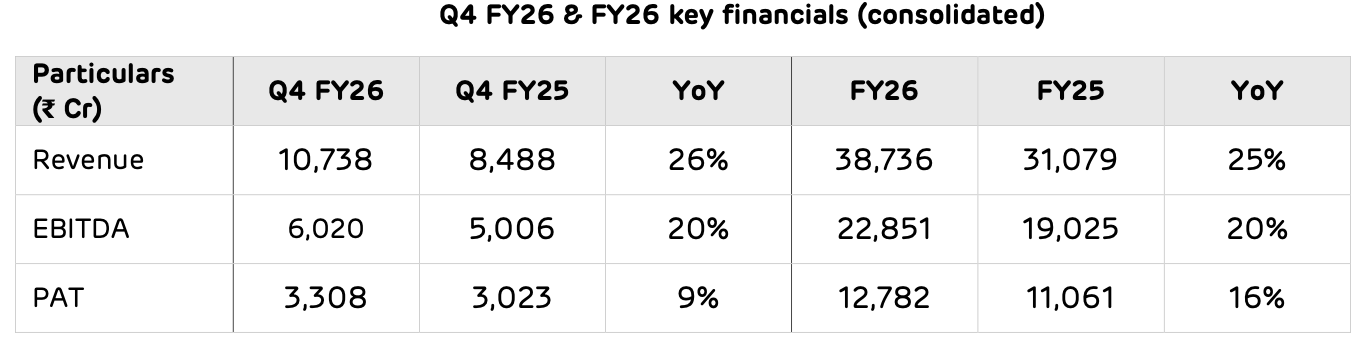

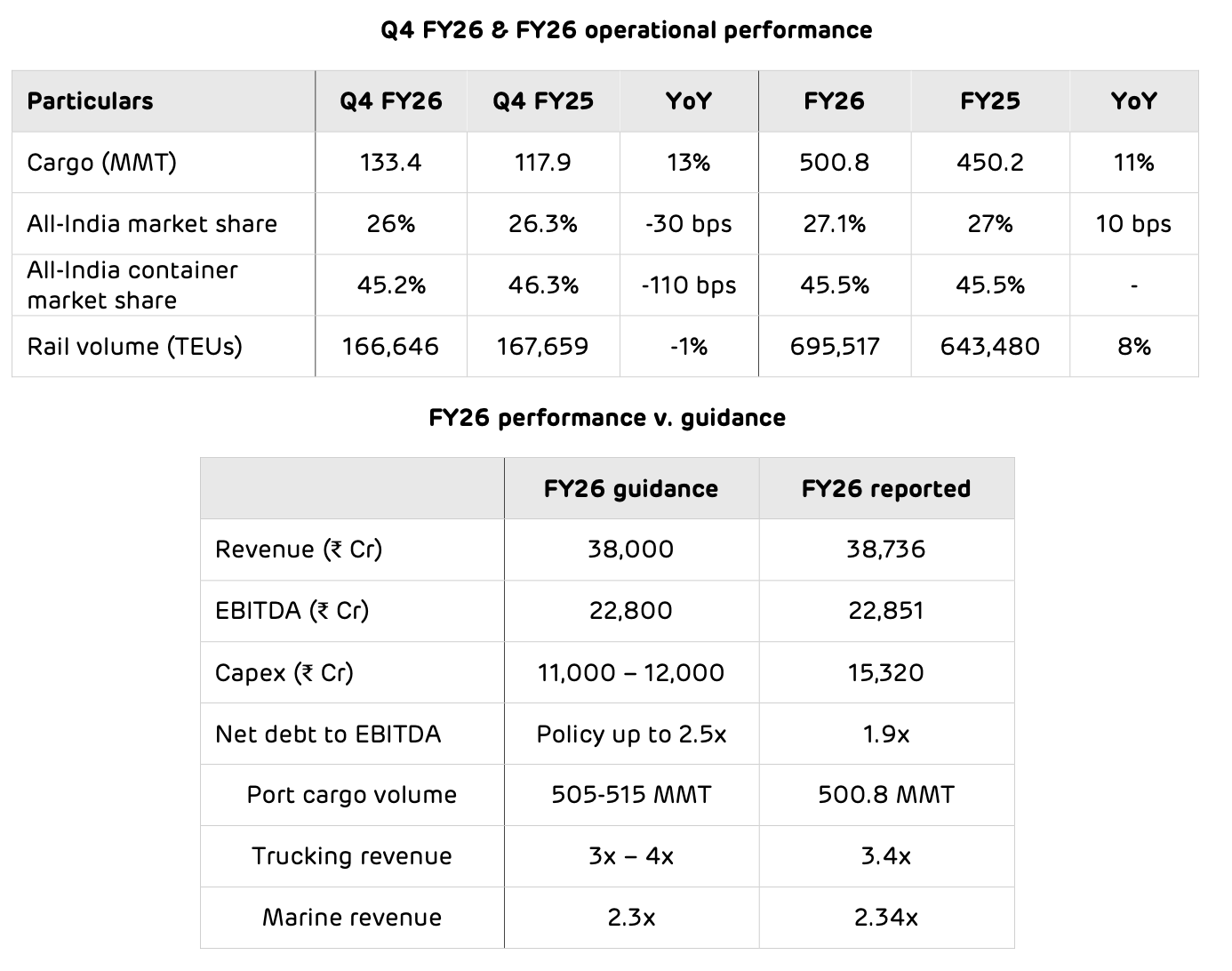

Domestic ports revenue grew 8% during Q4 FY26 (₹6,566 Cr vs. ₹6,062 Cr in Q4 FY25). For the full year, domestic ports revenue grew 13% (₹25,755 Cr vs. ₹22,740 Cr in FY25) led by 45.5% container market share. FY26 EBITDA was up by 14% (₹18,849 Cr in FY26 vs. ₹16,503 Cr in FY25). FY26 EBITDA margin stood at 73.2% (vs. 72.6% in FY25). As of 31st March 2026, domestic ports capacity stood at 653 MMT. FY26 RoCE at 23% (21% in FY25).

International ports delivered highest ever quarterly revenue at ₹1,422 Cr (+58% YoY, ₹901 Cr in Q4FY25), driven by NQXT addition and Colombo ramp up. International ports also delivered c.5x jump in Q4 FY26 EBITDA (₹597 Cr in Q4 FY26 vs. ₹131 Cr in Q4 FY25), led by all-time high 42% EBITDA margin (14.5% in Q4 FY25). During FY26, international ports revenue was up by 34% (₹4,539 Cr vs. ₹3,380 Cr in FY25). FY26 EBITDA margins stood at 28.6% vs. 13.7% in FY25. FY26 RoCE at 8%* (6% in FY25).

Logistics business delivered FY26 revenue growth of 55% YoY (₹4,478 Cr vs. ₹2,881 Cr in FY25), led by accelerated ramp up across asset-light Trucking services and asset-zero International Freight Network solutions. FY26 EBITDA grew by 34% (₹863 Cr vs. ₹642 Cr in FY25). Q4 FY26 revenue and EBITDA grew by 10% and 26% respectively. FY26 RoCE at 10% (6% in FY25).

During FY26, Marine operations delivered robust 134% YoY revenue (₹2,681 Cr vs. ₹1,144 Cr in FY25) and 125% EBITDA growth (₹1,357 Cr vs. ₹604 Cr in FY25), driven by offshore support vessel acquisitions in the Middle East, Africa, South Asia (MEASA) and India waters and backed by take- or-pay contracts with Tier-1 customers. Marine operations offer revenue visibility and deliver high capital efficiency. As of 31st March 2026, APSEZ’s marine vessel count stood at an all-time high of 136 vessels. FY26 EBITDA margin stood at 51% vs. 53% in FY25. During Q4FY26, revenue jumped 101% (₹726 Cr vs. ₹361 Cr in Q4 FY25). FY26 RoCE at 13% (13% in FY25).

Financial highlights

- ● Debt management: Gross debt at ₹55,103 Cr. Cash balance at ₹12,193 Cr. Net debt / EBITDA at

1.9x (proforma net debt / EBITDA calculated using TTM NQXT EBITDA at 1.8x)

- ● FY26 capex – ₹15,320 Cr (FY26 guidance ₹11,000 Cr – ₹12,000 Cr)

- ● New credit rating and rating affirmation: CareEdge Global’ assigned long-term foreign currency issuer rating of “CareEdge BBB+/Stable” to APSEZ. India Ratings and Research (Ind-Ra) reaffirmed APSEZ’s long-term issuer rating at “IND AAA” with “Stable” outlook. Ind-Ra has also reaffirmed APSEZ’s commercial paper rating at IND A1+

JCR assigned foreign currency and local currency long-term issuer credit rating of “A-/Stable” to APSEZ, a notch above India’s sovereign rating. Moody’s revised outlook to “Stable” from “Negative”, reaffirmed “Baa3” rating. ICRA reaffirmed “AAA/Stable”. Fitch Ratings revised outlook to “Stable” from “Negative”, affirmed rating at “BBB-“. S&P Global revised ratings outlook to “Positive” from “Negative” while reaffirming “BBB-“rating

Fitch Ratings upgraded NQXT’s long-term issuer default rating to “BBB-“ from “BB+” (“Stable” outlook)

- ● Capital optimization: Completed bond buyback program in March 2026, repurchasing total of US$199.57m (US$196.94m during early tender date and US$2.63m before expiration). Previously during the financial year, APSEZ completed a bond buyback program in August 2025, repurchasing total of US$386.03m (US$384.38m during early tender date and US$1.65m before expiration). Average debt maturity as on March 31, 2026 at 5.4 years (4.3 years as on March 31, 2025)

- ● Dividend: Board has proposed dividend of ₹7.5 dividend per share for FY26. The record date for the dividend is 12th June 2026