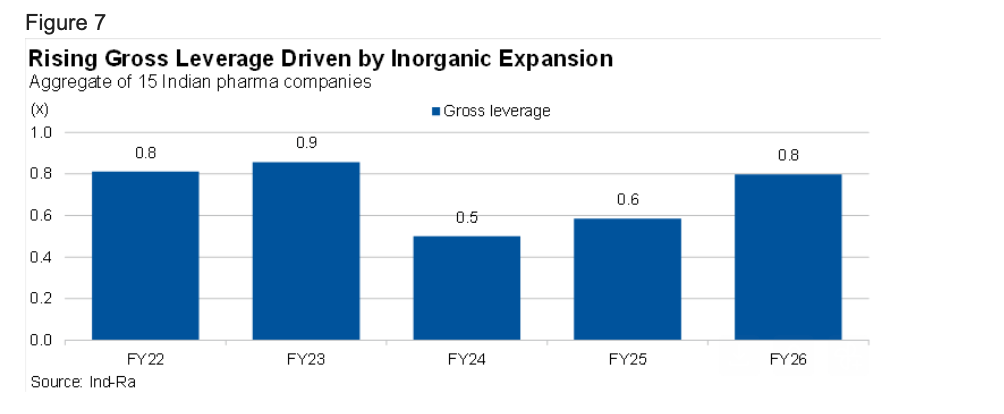

Mumbai: India Ratings and Research (Ind-Ra) believes Indian pharma companies’ strong balance sheets and sub-1x leverage profile (FY26: nearly 0.8x) provide headroom for sustained M&A-led growth, despite acquisition-led expansion, without materially weakening credit quality. This is reflected in largely stable rating actions, supported by double-digit revenue growth, around 70% gross margins, and above 25% EBITDA margins, alongside healthy cash flows. While working capital intensity has increased (cycle up about 10 days), balance sheets remain resilient. As one-off gains moderate and cost pressures emerge in FY27, Ind-Ra expects M&A to remain a key growth lever, with rating sensitivities centred on leverage, integration, and deleveraging execution.

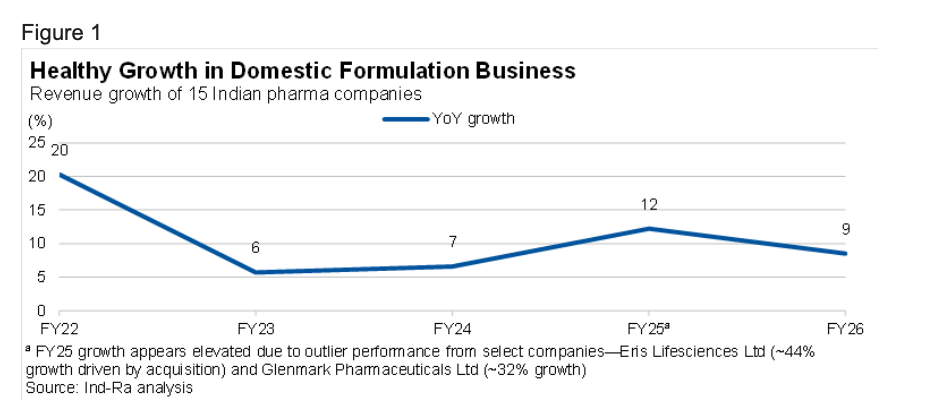

Healthy Growth in Domestic Formulation Business to Continue: Ind-Ra expects domestic revenues to grow 9%-10% yoy in FY27, supported by a sustained volume recovery, calibrated price increases, and continued new product launches. Domestic growth has remained resilient with mid-to-high single digit trajectory over FY24-FY26, normalising after an elevated FY25. Growth will be driven by chronic therapies—cardiac, anti-diabetic, vitamins / minerals / nutrients, respiratory and neuro/central nervous system—which continue to outpace the broader market. GLP-1 launches further strengthen the chronic mix. Acute therapies have also rebounded, supporting a broad-based demand recovery.

“We expect the sector to report around 10% yoy revenue growth in FY27, driven by a strong domestic performance and increasing traction in the contract development and manufacturing organisation (CDMO) segment. US growth is likely to remain under pressure due to the absence of gRevlimid and continued pricing headwinds. EBITDA margins should sustain at healthy levels, despite near-term cost pressures, supported by a favourable product mix, and currency and pass-through mechanisms. Strong balance sheets and liquidity will continue to support inorganic growth,” says Nishith Sanghvi, Director, Corporate Ratings, Ind-Ra.

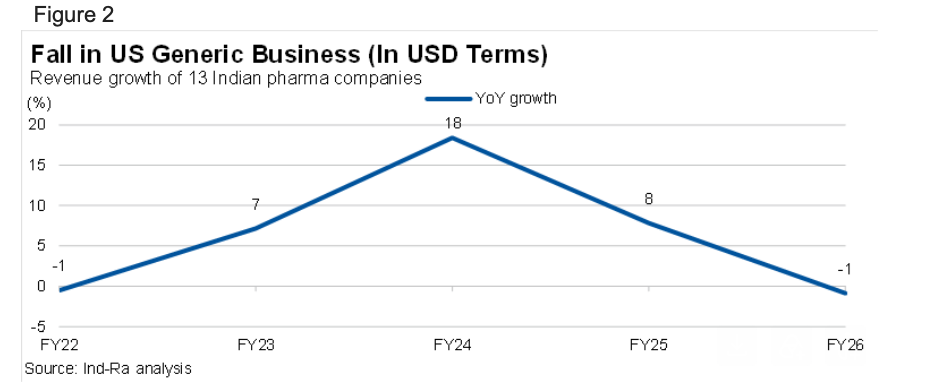

Fall in US Generics Business during FY26; Pressure Likely to Persist: US generics revenues declined marginally in FY26, after strong growth in FY24 (high-teens) and FY25 (high single digit), reflecting product-specific challenges and continued price erosion. The US continues to contribute over 35% to the sector revenues, underscoring its structural importance. Companies are accelerating investments in complex generics—injectables, transdermals, inhalants, nasal, and ophthalmics—to offset base portfolio erosion and sustain margins.

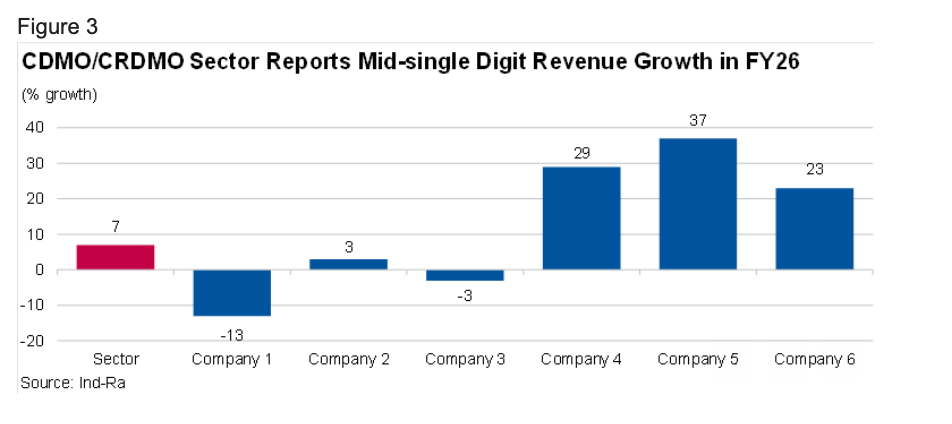

Healthy Growth Outlook for CDMO/Contract Research, Development, and Manufacturing Organisation (CRDMO): Ind-Ra believes growth visibility has improved meaningfully with recovery in biotech funding in 2026 and a build-up of late-stage pipelines. While FY26 growth was impacted by destocking and molecule attrition, recent order wins and deeper innovator engagement provide improved medium-term visibility. Ind-Ra expects mid-teens growth, driven by scale-up in high-value late-stage assets.

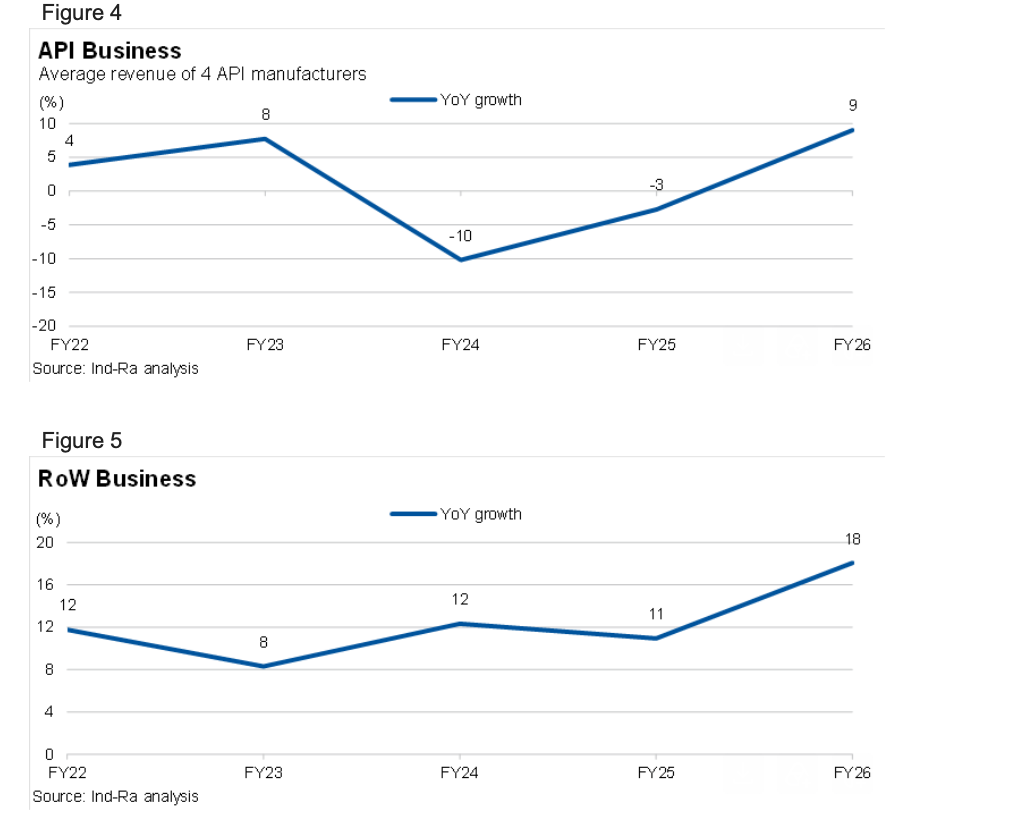

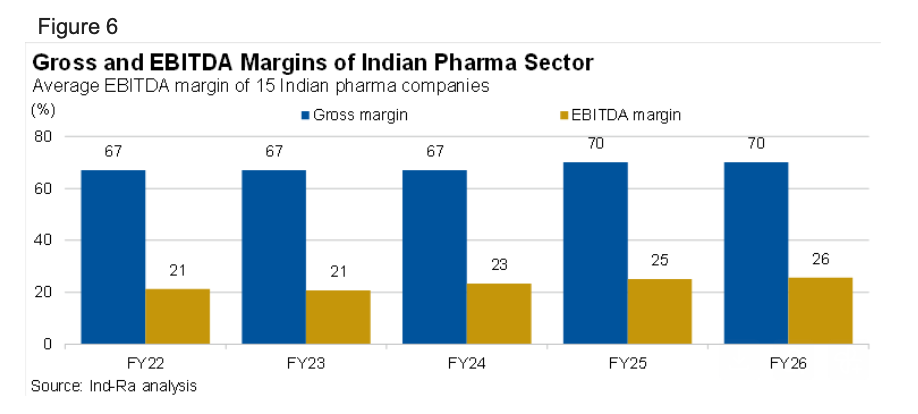

Volume-led Recovery in API and Growth in RoW Markets: Ind-Ra highlights that active pharmaceutical ingredient (API) growth has turned positive (FY26: nearly 9% yoy) after two years of decline, supported by volume recovery in regulated markets, although pricing remains weak. RoW markets have shown steady double-digit growth (FY26: high-teens), aided by currency tailwinds and focused geographic expansion, improving diversification of revenue mix.

Margins to Moderate in FY27 after Strong FY26: FY26 gross margins (about 70%) and EBITDA margins (above25%) benefited from a favourable product mix, one-off US opportunities, soft raw material costs, and operational efficiencies. While structural drivers remain intact, higher material and logistics costs (geopolitical factors) and absence of one-offs—particularly in 1HFY27—are likely to lead to some moderation in margins, although still above historical averages.

Leverage to Remain Comfortable, despite Inorganic Expansion: Ind-Ra observes that gross leverage increased to about 0.8x in FY26 from 0.5x in FY24, reflecting acquisition-led growth. Despite this, leverage remains conservative, supported by strong EBITDA generation. Ind-Ra expects the sector’s net leverage to remain below 1.5x on a sustained basis, preserving balance sheet strength even with continued M&A activity.

Recent M&A Activity and Rating Actions Underscore Inorganic Focus: The sector has witnessed continued acquisition activity aimed at strengthening product portfolios, expanding into complex generics/specialty therapies, and enhancing CDMO capabilities. This includes (i) acquisitions of branded domestic portfolios to scale chronic therapies, (ii) purchases of niche US/Europe assets to deepen complex generics presence, and (iii) bolt-on CDMO acquisitions to build late-stage capabilities.

Ind-Ra’s rating actions on such transactions have typically reflected a balanced view of (i) incremental leverage and (ii) medium-term strategic benefits. For instance, in cases of debt-funded domestic formulation acquisitions, Ind-Ra has affirmed ratings with a Stable Outlook, factoring in a moderate leverage increase offset by strong cash generation and expected scale benefits. In select transactions involving a large platform or overseas acquisitions, Ind-Ra has highlighted leverage and integration risks through Outlook revisions or rating sensitivities, while affirming the ratings, given comfortable starting balance sheets.

Ind-Ra has maintained a Stable rating Outlook on Torrent Pharmaceuticals Limited (debt rated at IND AA+/Stable), following its acquisition of JB Chemicals & Pharmaceuticals Limited.

Additionally, Ind-Ra has affirmed the rating on Eris Lifesciences Limited (debt rated at IND AA/Stable) in view of its multiple acquisitions.

Where acquisitions have strengthened therapeutic presence or added high-margin portfolios, Ind-Ra has factored in an expected improvement in business risk profiles, supporting rating stability despite near-term leverage increase. Conversely, in transactions with higher execution risk, Ind-Ra has emphasised deleveraging timelines, synergy realisation, and integration milestones as key rating triggers.